Maria Shepherd, President and Founder, Medi-Vantage12.02.19

For a long time, we all assumed Minnesota dominated the medical device industry worldwide, but is this true for the orthopedic surgical tools industry? And, which other geographical clusters lead1 in their contributions to the orthopedic industry?

Why This Is Important

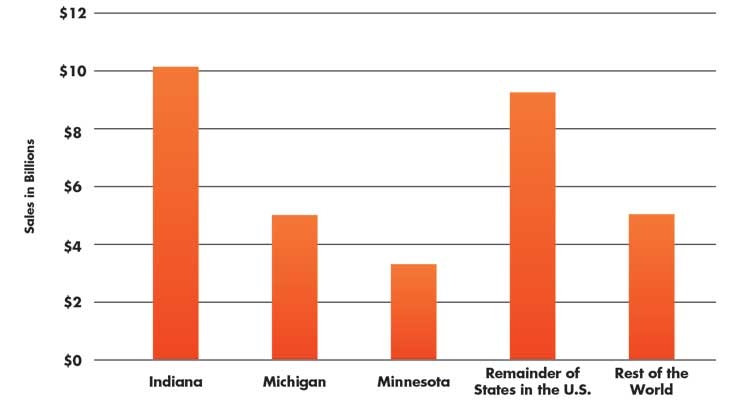

When an industry geographic location shifts, the ripple effect can be significant. Jobs are on the line as well as state revenues from taxes. Warsaw, Ind., claims it is the undisputed capital of the global orthopedic device industry (Table 1).2 There are some notable firsts that have come out of Warsaw. One of the world’s first orthopedic device businesses was founded in Warsaw by inventor Revra DePuy. Continuing innovation and entrepreneurship within the region ultimately led to dominance in the market. As a result, three of the world’s largest orthopedic manufacturers—DePuy (now owned by Johnson & Johnson), Zimmer, and Biomet (now owned by Zimmer)—have had their headquarters in Warsaw. As the orthopedics industry grew, a cluster developed of more than 20 orthopedic device manufacturers, service providers, and suppliers within Warsaw. Together, they can deliver the entire value chain of production and innovation required for the orthopedics surgical supplies industry.

Table 1: Orthopedic device sales for company based within the indicated region (2009).2

Orthopedics Medical Device Innovation Remains in Indiana

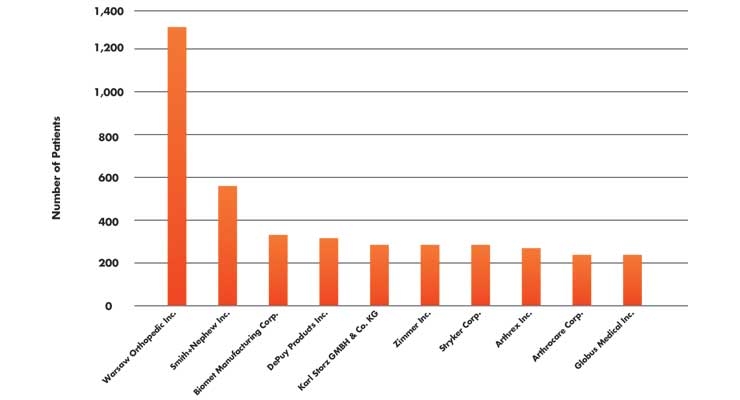

Patents are a sign of where the brainpower for the orthopedic medical device industry lives, and Indiana beats all the other states in America (Table 2).3

Table 2: Number of patents by orthopedic company (2002-2015)3

The companies in Warsaw are ground zero of a global network of customers, surgeons, suppliers, and research and development engineering expertise. This network brings value to all of Indiana because Warsaw is a manufacturing hub and a center of innovation and orthopedic product development activity. The orthopedics industry contributes to the increase seen in Indiana’s average income per capita.4 The annual income for Indiana’s medical device workforce exceeds an average $10,000 greater than Indiana or national averages. It has been estimated that the state of Indiana has seen an additional $581 million in economic activity due to the contributions of the orthopedic industry. The total statewide economic impact of Indiana’s orthopedic organizations was estimated at $3.7 million in 2009, approximately 1 percent of the state’s economic output.2

The Potential Impact of Digital Health?

Digital health is hot in Silicon Valley because this region is home to Google, Apple, Facebook, and a seemingly endless array of other related firms. Recently, an orthopedics/digital health partnership with Silicon Valley has been forming. As a result, the California/Indiana connection may benefit both regions, according to a report by Deloitte.5

In the report, Deloitte indicates that as the healthcare industry moves toward a value-based care model (which emphasizes prevention over treatment), future orthopedic technologies may alert clinical teams about pending health issues before they become symptomatic through the use of unobtrusive sensors. Digital health can change the medtech business model by driving collaboration with consumer-based technology companies to match the rapidly changing needs and expectations of their consumers, who are also our patients.

Another Deloitte report6 states the data collected from medical device hardware will eventually surpass the value of the device itself. In 20 years, when medtech hardware has become commoditized, it will be the ability to capture data through devices that will provide the most value to clinicians and patients. The data will be used to improve health, predict future issues, and engage patients to change behaviors that negatively affect their health.

Using an example specific to orthopedics, the report postulated orthopedic medical device manufacturers that develop artificial joints could incorporate diagnostic sensors in their technology, which could detect the early stages of joint degeneration. This type of technology might even assist patients in avoiding a joint replacement.

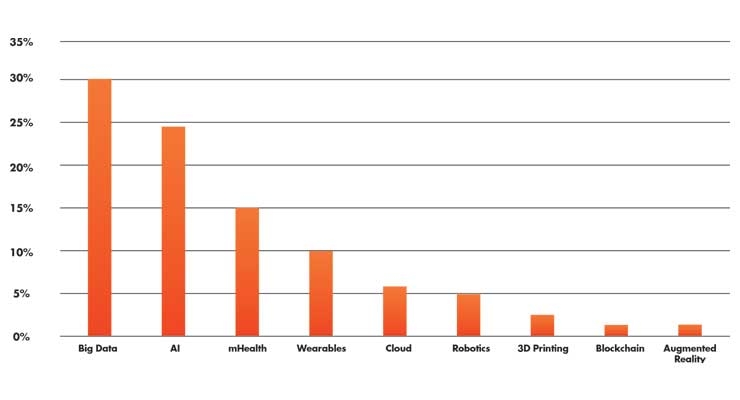

Digital technologies are in a constant state of flux and new applications emerge each year, while the base technologies remain the same. A Forbes article7 reported the results of a survey where respondents were asked to indicate the digital technology they believed would have the deepest impact on the healthcare industry in 2019 (Table 3).

Table 3: Responses from participants in a survey conducted by Forbes. Respondents were asked what digital technology they believed would most impact healthcare in 2019.7

Further cementing the evolution of orthopedic digital health technologies in California, the Digital Orthopaedics Conference San Francisco (DOCSF) meeting is taking place in January 2020. Its mission is to create an alliance of innovators and healthcare leaders to implement digital health solutions in musculoskeletal care.

The Medi-Vantage Perspective

Imagine the trillions of data points orthopedic medtech companies could have captured if knee and hip replacement technologies had already incorporated digital sensors that could track the relevant health issues an orthopedic patient could have. The time to start (if you haven’t already) is now; learn what orthopedic surgeons need to know from sensors that could be implanted into patients.

References

Maria Shepherd has more than 20 years of experience in medical device marketing in small startups and top-tier companies. After her industry career, including her role as VP of marketing for Oridion Medical, where she boosted the company valuation prior to its acquisition, director of marketing for Philips Medical, and senior management roles at Boston Scientific Corp., she founded Medi-Vantage. Medi-Vantage provides marketing, business strategy, and innovation research for the medical device, diagnostic, and digital health industries. The firm quantitatively and qualitatively sizes and segments opportunities, evaluates new technologies, provides marketing services, and assesses prospective acquisitions. Shepherd has taught marketing and product development courses and is a member of the Aligo Medtech Investment Committee (www.aligo.com). She can be reached at 855-343-3100. Visit her website at www.medi-vantage.com.

Why This Is Important

When an industry geographic location shifts, the ripple effect can be significant. Jobs are on the line as well as state revenues from taxes. Warsaw, Ind., claims it is the undisputed capital of the global orthopedic device industry (Table 1).2 There are some notable firsts that have come out of Warsaw. One of the world’s first orthopedic device businesses was founded in Warsaw by inventor Revra DePuy. Continuing innovation and entrepreneurship within the region ultimately led to dominance in the market. As a result, three of the world’s largest orthopedic manufacturers—DePuy (now owned by Johnson & Johnson), Zimmer, and Biomet (now owned by Zimmer)—have had their headquarters in Warsaw. As the orthopedics industry grew, a cluster developed of more than 20 orthopedic device manufacturers, service providers, and suppliers within Warsaw. Together, they can deliver the entire value chain of production and innovation required for the orthopedics surgical supplies industry.

Table 1: Orthopedic device sales for company based within the indicated region (2009).2

Orthopedics Medical Device Innovation Remains in Indiana

Patents are a sign of where the brainpower for the orthopedic medical device industry lives, and Indiana beats all the other states in America (Table 2).3

Table 2: Number of patents by orthopedic company (2002-2015)3

The companies in Warsaw are ground zero of a global network of customers, surgeons, suppliers, and research and development engineering expertise. This network brings value to all of Indiana because Warsaw is a manufacturing hub and a center of innovation and orthopedic product development activity. The orthopedics industry contributes to the increase seen in Indiana’s average income per capita.4 The annual income for Indiana’s medical device workforce exceeds an average $10,000 greater than Indiana or national averages. It has been estimated that the state of Indiana has seen an additional $581 million in economic activity due to the contributions of the orthopedic industry. The total statewide economic impact of Indiana’s orthopedic organizations was estimated at $3.7 million in 2009, approximately 1 percent of the state’s economic output.2

The Potential Impact of Digital Health?

Digital health is hot in Silicon Valley because this region is home to Google, Apple, Facebook, and a seemingly endless array of other related firms. Recently, an orthopedics/digital health partnership with Silicon Valley has been forming. As a result, the California/Indiana connection may benefit both regions, according to a report by Deloitte.5

In the report, Deloitte indicates that as the healthcare industry moves toward a value-based care model (which emphasizes prevention over treatment), future orthopedic technologies may alert clinical teams about pending health issues before they become symptomatic through the use of unobtrusive sensors. Digital health can change the medtech business model by driving collaboration with consumer-based technology companies to match the rapidly changing needs and expectations of their consumers, who are also our patients.

Another Deloitte report6 states the data collected from medical device hardware will eventually surpass the value of the device itself. In 20 years, when medtech hardware has become commoditized, it will be the ability to capture data through devices that will provide the most value to clinicians and patients. The data will be used to improve health, predict future issues, and engage patients to change behaviors that negatively affect their health.

Using an example specific to orthopedics, the report postulated orthopedic medical device manufacturers that develop artificial joints could incorporate diagnostic sensors in their technology, which could detect the early stages of joint degeneration. This type of technology might even assist patients in avoiding a joint replacement.

Digital technologies are in a constant state of flux and new applications emerge each year, while the base technologies remain the same. A Forbes article7 reported the results of a survey where respondents were asked to indicate the digital technology they believed would have the deepest impact on the healthcare industry in 2019 (Table 3).

Table 3: Responses from participants in a survey conducted by Forbes. Respondents were asked what digital technology they believed would most impact healthcare in 2019.7

Further cementing the evolution of orthopedic digital health technologies in California, the Digital Orthopaedics Conference San Francisco (DOCSF) meeting is taking place in January 2020. Its mission is to create an alliance of innovators and healthcare leaders to implement digital health solutions in musculoskeletal care.

The Medi-Vantage Perspective

Imagine the trillions of data points orthopedic medtech companies could have captured if knee and hip replacement technologies had already incorporated digital sensors that could track the relevant health issues an orthopedic patient could have. The time to start (if you haven’t already) is now; learn what orthopedic surgeons need to know from sensors that could be implanted into patients.

References

- http://bit.ly/odt191201

- http://bit.ly/odt191202

- http://bit.ly/odt191203

- http://bit.ly/odt191204

- http://bit.ly/odt191205

- http://bit.ly/odt191206

- http://bit.ly/odt191207

Maria Shepherd has more than 20 years of experience in medical device marketing in small startups and top-tier companies. After her industry career, including her role as VP of marketing for Oridion Medical, where she boosted the company valuation prior to its acquisition, director of marketing for Philips Medical, and senior management roles at Boston Scientific Corp., she founded Medi-Vantage. Medi-Vantage provides marketing, business strategy, and innovation research for the medical device, diagnostic, and digital health industries. The firm quantitatively and qualitatively sizes and segments opportunities, evaluates new technologies, provides marketing services, and assesses prospective acquisitions. Shepherd has taught marketing and product development courses and is a member of the Aligo Medtech Investment Committee (www.aligo.com). She can be reached at 855-343-3100. Visit her website at www.medi-vantage.com.