Maria Shepherd, President and Founder, Medi-Vantage02.08.21

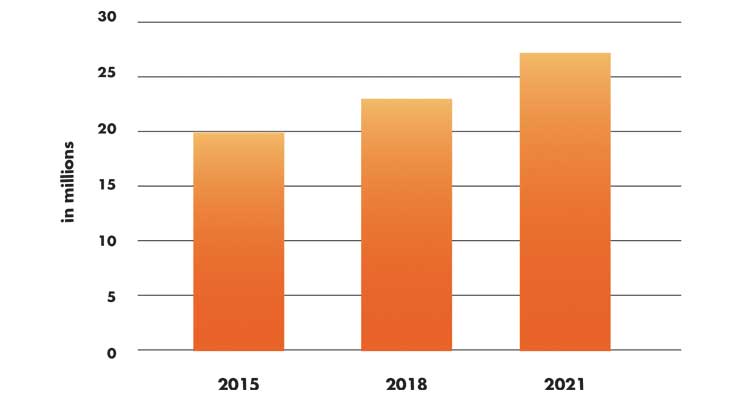

The long, strange trip of 2020’s impact on healthcare has combined the forces of the pandemic, orthopedic-surgeon-owned ASCs, and decimated hospital capital expenditure budgets to cause radical change in ASCs delivery and the purchase of medical devices and equipment. Orthopedic ASCs have embraced a strategy to focus on low-risk procedures (e.g., hip and knee replacements, sports medicine), with lower complication rates in an out-of-hospital setting. The cost of the procedure is considerably less, with charges 35 to 50 percent lower than hospitals.1 It is a huge savings for U.S. healthcare, by a projected $40 billion a year. This is the engine driving ASC growth (Table 1).

Table 1: ASC procedure rate growth [2015–2021 (forecasted)]1

Why This Is Important

By 2017, ASCs penetrated more than 50 percent of all outpatient surgeries. This is an increase from a 32 percent penetration rate in 2005, and is expected to grow by an average six percent per year through 2021, a significant increase from the 4 percent CAGRs seen between 2015 to 2018. Cardiology, orthopedic, and spine procedures are expected to grow at the greatest rates. Since ASCs are more price sensitive, pricing pressure is increased for medtech due to the lower reimbursement rates for ASCs. ASC-based physicians (often owners) are far more price sensitive than hospital-based physicians, who may not have the same level of skin in the game. It’s not easy to create a sales plan for ASCs because they are smaller, often independent, with lower revenue potential and sometimes located outside of major metropolitan areas. This increases the cost of distribution and selling, making medtech marketing and sales plans more expensive.

With 50 percent of all outpatient surgeries performed at ASCs, we recommend our orthopedic device clients develop a separate ASC strategy for their commercialization and product development plans, especially if the technology is considered disruptive.

During a recent virtual event,2 experts shared important trends and concepts for orthopedic surgery, joint replacements, sports medicine, and ASCs. Expect consolidation in ASCs, but not with the obvious suspects like the big ASC chains. Many orthopedic surgeons want to remain independent and will consider consolidation with other physician groups. Also to be considered are hospital joint ventures where ASCs can add value.

Patients are still concerned about elective procedure health risk in hospitals. ASCs can be nimble and provide virtual scheduling, check-ins, post-op home care, and physical therapy. Telehealth and online patient communications have been critical in guaranteeing patients receive appropriate care. Orthopedic surgeons are more likely to embrace telehealth now that the platforms have become so much more efficient and telehealth reimbursement has improved.

Orthopedic ASCs Have Room to Grow

Single specialty orthopedic surgery ASCs are still low in number. In 2018, there were only 33 single specialty orthopedic surgery ASCs in the U.S., according to a report to the U.S. Congress by MEDPAC.3 However, when considering ASCs with more than two specialties, there were more orthopedic ASCs. In addition, this number is expected to grow.

What Are Other Medtech Leaders Doing?

There are many strategies to consider for ASCs. The best strategies combine the strengths of your product with the weakness of your key competitors. Many medtech managers’ teams start with the strength/weakness algorithm and then augment those strategies by developing programs like reduced-cost service models and a simplified product mix. Your team should also consider customized services and partnerships such as technological support for scheduling, operating room utilization, administration, and staffing. Staffing has become a huge issue in hospitals and ASCs, and anything your product can do to reduce the level of staff needed in the OR by simplifying the procedure brings value.

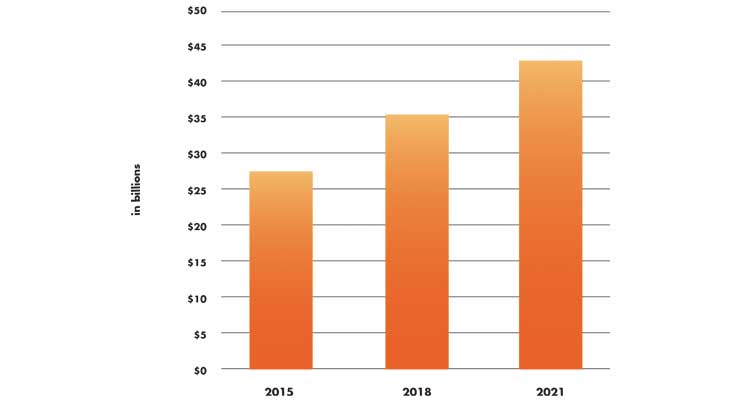

The value of ASC procedures is growing along with their number (Table 2). Hospital leadership and payers have been put on high alert as the most profitable surgical procedures are skimmed off to ASCs and outpatient centers. Payers have directed procedures to ASCs by lowering reimbursements for hospitals and decreasing patient copayments for outpatient procedures. Many hospital systems are acquiring ASCs to regain a piece of the business they have lost, and it is reported that approximately 25 percent of ASCs now have hospitals as shareholders. Others are moving to the physician-as-a-hospital-employee business model by acquiring physician practices to re-direct referral patterns. And of course, payers want to push the trend to lower-cost healthcare locations, and some have also become part of ASC ownership.

Table 2: Revenues from ASC procedures [2015–2021 (forecasted)]1

While the majority of ASCs are still solely owned by physicians,4 giving physicians the benefit of profit and maximum control, it also brings challenges in management and contracting—skills not taught in medical school. Many have tried a joint-venture model, combining physician owners, ASC management companies, and hospitals in an effort to balance physician control and management expertise.

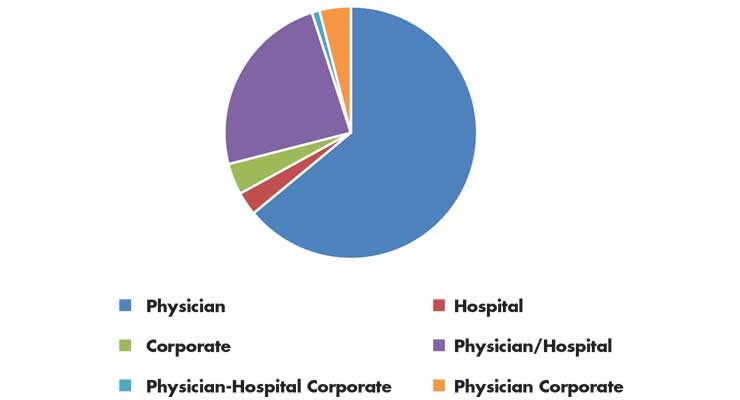

ASC ownership is very attractive to physicians. A recent survey1 revealed almost 60 percent of physicians not affiliated with an ASC are interested in investigating a practice at an ASC. Surgeons want a piece of the action by owning ASC equity, increased control over their surgery schedules, and a decrease in the bureaucracy they experience in a hospital environment (Table 3).

Table 3: ASC ownership5

Payers are helping push procedures to ASCs by lowering provider reimbursements for hospitals and reducing patient copayment for procedures performed at outpatient centers.

By 2023, growth in procedures performed in ASCs will fast-track, driven by cost burdens, approval by CMS to reimburse even more procedures for ASCs, the surge in results-based care standards, and preference by physicians and patients for outpatient surgery.

Adjust Sales and Product Development Strategies

The entrenched business model at most medical device companies is focused on large, academic hospital systems, with high patient volumes, key opinion leaders who can handle complex procedures, and familiar buying behaviors. ASCs are smaller, more agile, and have more basic needs—typical hospital commercialization models and products are often too costly and overly complex.

Many physicians at ASCs are owners and have much more influence over purchasing decisions for medical devices as compared with their surgeon peers working in hospitals. ASCs are reimbursed less by payers for the same procedure performed in the hospital, which causes relentless pressure to decrease costs and increase efficiency. ASCs can and will switch to another manufacturer if that medtech company can provide a value proposition that supports that decision. ASC physicians are price sensitive and have high expectations for reduced prices compared to what hospitals pay for the same equipment. Further, ASC physicians are more receptive to use innovative procurement models as long as the benefit is clear.

The Medi-Vantage Perspective

More than 50 percent of our research is performed with the buyers in hospitals and ASCs and we find their expectations of medical device companies are very different. For example, ASCs value technical support and information on payer reimbursement. Hospital administrators want OR coverage for inventory-heavy procedures, provided by orthopedics reps with technical knowledge on how to assemble and implant the device. These are the details surrounding every specialty that must inform your product development.

References

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, including her role as vice president of marketing for Oridion Medical where she boosted the company valuation prior to its acquisition by Medtronic, director of marketing for Philips Medical, and senior management roles at Boston Scientific Corp., she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. The firm quantitatively and qualitatively sizes and segments opportunities, evaluates new technologies, provides marketing services, and assesses prospective acquisitions. Shepherd has taught marketing and product development courses, speaks regularly at medtech conferences, and can be reached at mshepherd@medi-vantage. Visit her website at www.medi-vantage.com.

Table 1: ASC procedure rate growth [2015–2021 (forecasted)]1

Why This Is Important

By 2017, ASCs penetrated more than 50 percent of all outpatient surgeries. This is an increase from a 32 percent penetration rate in 2005, and is expected to grow by an average six percent per year through 2021, a significant increase from the 4 percent CAGRs seen between 2015 to 2018. Cardiology, orthopedic, and spine procedures are expected to grow at the greatest rates. Since ASCs are more price sensitive, pricing pressure is increased for medtech due to the lower reimbursement rates for ASCs. ASC-based physicians (often owners) are far more price sensitive than hospital-based physicians, who may not have the same level of skin in the game. It’s not easy to create a sales plan for ASCs because they are smaller, often independent, with lower revenue potential and sometimes located outside of major metropolitan areas. This increases the cost of distribution and selling, making medtech marketing and sales plans more expensive.

With 50 percent of all outpatient surgeries performed at ASCs, we recommend our orthopedic device clients develop a separate ASC strategy for their commercialization and product development plans, especially if the technology is considered disruptive.

During a recent virtual event,2 experts shared important trends and concepts for orthopedic surgery, joint replacements, sports medicine, and ASCs. Expect consolidation in ASCs, but not with the obvious suspects like the big ASC chains. Many orthopedic surgeons want to remain independent and will consider consolidation with other physician groups. Also to be considered are hospital joint ventures where ASCs can add value.

Patients are still concerned about elective procedure health risk in hospitals. ASCs can be nimble and provide virtual scheduling, check-ins, post-op home care, and physical therapy. Telehealth and online patient communications have been critical in guaranteeing patients receive appropriate care. Orthopedic surgeons are more likely to embrace telehealth now that the platforms have become so much more efficient and telehealth reimbursement has improved.

Orthopedic ASCs Have Room to Grow

Single specialty orthopedic surgery ASCs are still low in number. In 2018, there were only 33 single specialty orthopedic surgery ASCs in the U.S., according to a report to the U.S. Congress by MEDPAC.3 However, when considering ASCs with more than two specialties, there were more orthopedic ASCs. In addition, this number is expected to grow.

What Are Other Medtech Leaders Doing?

There are many strategies to consider for ASCs. The best strategies combine the strengths of your product with the weakness of your key competitors. Many medtech managers’ teams start with the strength/weakness algorithm and then augment those strategies by developing programs like reduced-cost service models and a simplified product mix. Your team should also consider customized services and partnerships such as technological support for scheduling, operating room utilization, administration, and staffing. Staffing has become a huge issue in hospitals and ASCs, and anything your product can do to reduce the level of staff needed in the OR by simplifying the procedure brings value.

The value of ASC procedures is growing along with their number (Table 2). Hospital leadership and payers have been put on high alert as the most profitable surgical procedures are skimmed off to ASCs and outpatient centers. Payers have directed procedures to ASCs by lowering reimbursements for hospitals and decreasing patient copayments for outpatient procedures. Many hospital systems are acquiring ASCs to regain a piece of the business they have lost, and it is reported that approximately 25 percent of ASCs now have hospitals as shareholders. Others are moving to the physician-as-a-hospital-employee business model by acquiring physician practices to re-direct referral patterns. And of course, payers want to push the trend to lower-cost healthcare locations, and some have also become part of ASC ownership.

Table 2: Revenues from ASC procedures [2015–2021 (forecasted)]1

While the majority of ASCs are still solely owned by physicians,4 giving physicians the benefit of profit and maximum control, it also brings challenges in management and contracting—skills not taught in medical school. Many have tried a joint-venture model, combining physician owners, ASC management companies, and hospitals in an effort to balance physician control and management expertise.

ASC ownership is very attractive to physicians. A recent survey1 revealed almost 60 percent of physicians not affiliated with an ASC are interested in investigating a practice at an ASC. Surgeons want a piece of the action by owning ASC equity, increased control over their surgery schedules, and a decrease in the bureaucracy they experience in a hospital environment (Table 3).

Table 3: ASC ownership5

Payers are helping push procedures to ASCs by lowering provider reimbursements for hospitals and reducing patient copayment for procedures performed at outpatient centers.

By 2023, growth in procedures performed in ASCs will fast-track, driven by cost burdens, approval by CMS to reimburse even more procedures for ASCs, the surge in results-based care standards, and preference by physicians and patients for outpatient surgery.

Adjust Sales and Product Development Strategies

The entrenched business model at most medical device companies is focused on large, academic hospital systems, with high patient volumes, key opinion leaders who can handle complex procedures, and familiar buying behaviors. ASCs are smaller, more agile, and have more basic needs—typical hospital commercialization models and products are often too costly and overly complex.

Many physicians at ASCs are owners and have much more influence over purchasing decisions for medical devices as compared with their surgeon peers working in hospitals. ASCs are reimbursed less by payers for the same procedure performed in the hospital, which causes relentless pressure to decrease costs and increase efficiency. ASCs can and will switch to another manufacturer if that medtech company can provide a value proposition that supports that decision. ASC physicians are price sensitive and have high expectations for reduced prices compared to what hospitals pay for the same equipment. Further, ASC physicians are more receptive to use innovative procurement models as long as the benefit is clear.

The Medi-Vantage Perspective

More than 50 percent of our research is performed with the buyers in hospitals and ASCs and we find their expectations of medical device companies are very different. For example, ASCs value technical support and information on payer reimbursement. Hospital administrators want OR coverage for inventory-heavy procedures, provided by orthopedics reps with technical knowledge on how to assemble and implant the device. These are the details surrounding every specialty that must inform your product development.

References

- bit.ly/odt210101

- bit.ly/odt210102

- bit.ly/odt210103

- bit.ly/odt210104

- ASCA Owner Salary and Benefits Survey (2017)

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, including her role as vice president of marketing for Oridion Medical where she boosted the company valuation prior to its acquisition by Medtronic, director of marketing for Philips Medical, and senior management roles at Boston Scientific Corp., she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. The firm quantitatively and qualitatively sizes and segments opportunities, evaluates new technologies, provides marketing services, and assesses prospective acquisitions. Shepherd has taught marketing and product development courses, speaks regularly at medtech conferences, and can be reached at mshepherd@medi-vantage. Visit her website at www.medi-vantage.com.