Maria Shepherd, President and Founder, Medi-Vantage03.16.21

You can’t discuss orthopedic medical and surgical supply costs without considering both hospitals and ambulatory surgery centers (ASCs). According to recently published data,1 supply costs (including medical devices) are one of the greatest expenses for healthcare facilities, after labor and administrative expenses. In total, supply budgets equal approximately 25-33 percent of the medical and surgical operating expenses at U.S. hospitals. It has also been reported, however, supplies contribute to 15 percent of total hospital expenses, on average, but can go as high as 30 to 40 percent in healthcare institutions with a high case-mix index, such as surgery-intensive hospitals.2

According to a 2018 article, U.S. hospitals spent approximately $200 billion on medtech,3 or about 6 percent of the estimated U.S. healthcare spend of $3.81 trillion in 2019.4 These figures are pre-COVID for medical and implantable devices, and do not include pharmaceuticals. Now, with many procedures shifting to ASCs, the spend on medical devices is swinging in the same direction. There are many drivers to this shift, and one of the most influential is the new CPT/HCPCS codes for ASC procedures and the phase out of the Inpatient Only List over the next three years. It is estimated that, by then, 1,700 procedures will be covered by the Centers for Medicare & Medicaid Services (CMS) for ASCs.5

Why This Is Important

It is a brave new world for medical device companies. For example, CMS announced this past December the Stryker SpineJack implantable fracture reduction system qualified for the Transitional Pass-Through (TPT) payment in the 2021 Medicare Hospital Outpatient Prospective Payment System.6 The Stryker SpineJack system has now become one of only 11 medical devices to receive TPT status since 2016.

The TPT designation provides supplemental payment for new medical devices that demonstrate a substantial clinical improvement over existing technology. This new payment category is meant to provide Americans with access to innovative medical technologies while cost data, which is still required, is collected. The TPT payment—effective as of Jan. 1, 2021—will provide outpatient facilities with an incremental CMS payment for the Stryker SpineJack System for up to three years. This announcement came just after CMS awarded the SpineJack System the New Technology Add-on Payment (NTAP), which provides additional payment in the hospital inpatient setting.

So, while orthopedic ASCs are skimming off low-risk procedures, such as hip and knee replacements that have lower complication rates in an out-of-hospital setting, hospital inpatient settings are also rewarded. The cost of the procedure in an ASC is considerably less, by charges that are 35 to 50 percent lower than hospitals.7

That, however, is not all orthopedic ASCs are doing. They are also moving the needle on physician preference items (PPIs). With many physicians at ASCs operating as owners and surgeons, they have developed much more influence over purchasing decisions for medical devices. Further, the environment has changed. For example, in 2007, orthopedic surgeons (employed by hospitals) had a higher level of PPI (61 percent) used for implants.8 Fast forward to 2019 and new data show the supply chain for spinal fusion devices was estimated to have been reduced by 40 percent.9 This is understandable since standardization reduces working capital, which increases profitability. This has become a critical variable because ASCs are reimbursed at far lower rates by payers for the same procedure conducted in the hospital.

It is estimated that from 2014 to 2018, medical and surgical supply costs grew by a 7 percent CAGR in U.S. hospitals (Table 1). In comparison, total hospital supply costs rose by an estimated 6 percent CAGR during the same period. This is big money, and it is good news for the medical products industry. In 2018, medical and surgical supply costs were calculated at $27.4 million on average per hospital. If the same growth continues, the total by 2025 will rise to $44 million annually per healthcare facility.

Table 1: 2018 Medical and Surgical Supply Costs vs. Net Patient Revenue by Institution1

The 50:50 Split

The squeeze on hospital outpatient procedures means they are also becoming more cost-sensitive and it is important to know where to focus new orthopedic product development efforts. Hospitals with greater than 250 beds average $56 million in medical and surgical supply costs. In 2018, medium-sized hospitals (101-250 beds) were reported to spend approximately $14.4 million on medical and surgical supplies. This means hospitals with bed sizes greater than 250 spend almost four times the amount of the medium-sized facilities (Table 2).

Table 2: Average Medical and Surgical Supply Spend by Hospital Bed Count1

The Shifting Supply Chain

Growth in the U.S. ASC market is a result of increased focus on reduction of healthcare costs and diverted healthcare spending to these ASCs. Development of a new ASC requires significant capital investment to build new facilities or upgrade existing ones to remain competitive.10 The change in the number of ASCs is an indicator of the willingness of the financial community to meet the needs of an ASC’s ability to raise capital. The number of ASCs grew significantly over the past decade, from 5,253 in 2013 to 5,717 in 2018.11

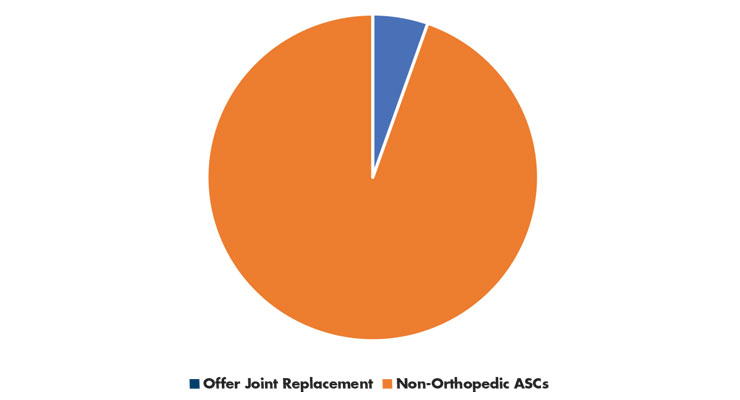

In 2018, most ASCs that billed CMS specialized in a single clinical area. Gastroenterology and ophthalmology (both 21 percent of ASCs) were the most frequently reported. In 2021, greater than 500 ASCs were reported to offer joint replacement surgery12 out of the 9,280 ASCs reportedly in the U.S.11 (Table 3). Expect growth in ASCs offering joint replacement to catch up with this new surge in ASC numbers.

Table 3: ASC Specialization11,12

The Medi-Vantage Perspective

The shift from hospitals to ASCs will have a substantial impact on the U.S. orthopedic medical device market. ASCs will perform an estimated 68 percent of orthopedic surgeries by the mid-2020s, according to a recently published market research report.13 While most ASCs adhere to high quality standards, many ASCs in our research are late adopters and purchase refurbished capital equipment to manage the lower reimbursements they are getting for commonly performed procedures. This doesn’t mean a medical device strategy targeting ASCs will be unsuccessful. However, the products to be developed for a lower reimbursement environment must have carefully selected marketing requirements to be sure they meet the price sensitivity of orthopedic ASCs and outpatient departments. It is this added set of unmet needs that will make your orthopedic ASC-targeted device robust and successful.

References

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. Shepherd can be reached at mshepherd@medi-vantage.com. Visit her website at www.medi-vantage.com.

According to a 2018 article, U.S. hospitals spent approximately $200 billion on medtech,3 or about 6 percent of the estimated U.S. healthcare spend of $3.81 trillion in 2019.4 These figures are pre-COVID for medical and implantable devices, and do not include pharmaceuticals. Now, with many procedures shifting to ASCs, the spend on medical devices is swinging in the same direction. There are many drivers to this shift, and one of the most influential is the new CPT/HCPCS codes for ASC procedures and the phase out of the Inpatient Only List over the next three years. It is estimated that, by then, 1,700 procedures will be covered by the Centers for Medicare & Medicaid Services (CMS) for ASCs.5

Why This Is Important

It is a brave new world for medical device companies. For example, CMS announced this past December the Stryker SpineJack implantable fracture reduction system qualified for the Transitional Pass-Through (TPT) payment in the 2021 Medicare Hospital Outpatient Prospective Payment System.6 The Stryker SpineJack system has now become one of only 11 medical devices to receive TPT status since 2016.

The TPT designation provides supplemental payment for new medical devices that demonstrate a substantial clinical improvement over existing technology. This new payment category is meant to provide Americans with access to innovative medical technologies while cost data, which is still required, is collected. The TPT payment—effective as of Jan. 1, 2021—will provide outpatient facilities with an incremental CMS payment for the Stryker SpineJack System for up to three years. This announcement came just after CMS awarded the SpineJack System the New Technology Add-on Payment (NTAP), which provides additional payment in the hospital inpatient setting.

So, while orthopedic ASCs are skimming off low-risk procedures, such as hip and knee replacements that have lower complication rates in an out-of-hospital setting, hospital inpatient settings are also rewarded. The cost of the procedure in an ASC is considerably less, by charges that are 35 to 50 percent lower than hospitals.7

That, however, is not all orthopedic ASCs are doing. They are also moving the needle on physician preference items (PPIs). With many physicians at ASCs operating as owners and surgeons, they have developed much more influence over purchasing decisions for medical devices. Further, the environment has changed. For example, in 2007, orthopedic surgeons (employed by hospitals) had a higher level of PPI (61 percent) used for implants.8 Fast forward to 2019 and new data show the supply chain for spinal fusion devices was estimated to have been reduced by 40 percent.9 This is understandable since standardization reduces working capital, which increases profitability. This has become a critical variable because ASCs are reimbursed at far lower rates by payers for the same procedure conducted in the hospital.

It is estimated that from 2014 to 2018, medical and surgical supply costs grew by a 7 percent CAGR in U.S. hospitals (Table 1). In comparison, total hospital supply costs rose by an estimated 6 percent CAGR during the same period. This is big money, and it is good news for the medical products industry. In 2018, medical and surgical supply costs were calculated at $27.4 million on average per hospital. If the same growth continues, the total by 2025 will rise to $44 million annually per healthcare facility.

Table 1: 2018 Medical and Surgical Supply Costs vs. Net Patient Revenue by Institution1

The 50:50 Split

The squeeze on hospital outpatient procedures means they are also becoming more cost-sensitive and it is important to know where to focus new orthopedic product development efforts. Hospitals with greater than 250 beds average $56 million in medical and surgical supply costs. In 2018, medium-sized hospitals (101-250 beds) were reported to spend approximately $14.4 million on medical and surgical supplies. This means hospitals with bed sizes greater than 250 spend almost four times the amount of the medium-sized facilities (Table 2).

Table 2: Average Medical and Surgical Supply Spend by Hospital Bed Count1

The Shifting Supply Chain

Growth in the U.S. ASC market is a result of increased focus on reduction of healthcare costs and diverted healthcare spending to these ASCs. Development of a new ASC requires significant capital investment to build new facilities or upgrade existing ones to remain competitive.10 The change in the number of ASCs is an indicator of the willingness of the financial community to meet the needs of an ASC’s ability to raise capital. The number of ASCs grew significantly over the past decade, from 5,253 in 2013 to 5,717 in 2018.11

In 2018, most ASCs that billed CMS specialized in a single clinical area. Gastroenterology and ophthalmology (both 21 percent of ASCs) were the most frequently reported. In 2021, greater than 500 ASCs were reported to offer joint replacement surgery12 out of the 9,280 ASCs reportedly in the U.S.11 (Table 3). Expect growth in ASCs offering joint replacement to catch up with this new surge in ASC numbers.

Table 3: ASC Specialization11,12

The Medi-Vantage Perspective

The shift from hospitals to ASCs will have a substantial impact on the U.S. orthopedic medical device market. ASCs will perform an estimated 68 percent of orthopedic surgeries by the mid-2020s, according to a recently published market research report.13 While most ASCs adhere to high quality standards, many ASCs in our research are late adopters and purchase refurbished capital equipment to manage the lower reimbursements they are getting for commonly performed procedures. This doesn’t mean a medical device strategy targeting ASCs will be unsuccessful. However, the products to be developed for a lower reimbursement environment must have carefully selected marketing requirements to be sure they meet the price sensitivity of orthopedic ASCs and outpatient departments. It is this added set of unmet needs that will make your orthopedic ASC-targeted device robust and successful.

References

- bit.ly/odt210301

- bit.ly/odt210302

- bit.ly/odt210303

- bit.ly/odt210304

- bit.ly/odt210305

- bit.ly/odt210306

- bit.ly/odt210307

- bit.ly/odt210308

- bit.ly/odt210309

- bit.ly/odt210310

- bit.ly/odt210311

- bit.ly/odt210313

- bit.ly/odt210314

Maria Shepherd has more than 20 years of leadership experience in medical device/life-science marketing in small startups and top-tier companies. After her industry career, she founded Medi-Vantage. Medi-Vantage provides marketing and business strategy and innovation research for the medical device industry. Shepherd can be reached at mshepherd@medi-vantage.com. Visit her website at www.medi-vantage.com.