Michael Barbella, Managing Editor12.05.22

The worldwide orthopedic prosthetic devices market is set to sustain nearly double-digit growth this decade.

Custom Market Insights estimates the market value at approximately $1.96 billion this year and expects it to expand 9.5% annually to reach $3.97 billion by 2030, thanks to a projected increase in accidental injuries and trauma cases. Accidental injuries and trauma can result from sports injuries, medical complications, road accidents, and work-related injuries. Most of these accidents require prosthetics or amputations device to replace the lost body part. Around 2.1 million U.S. residents are living with limb loss, and that number is expected to double by 2050. Nearly 185,000 U.S. residents undergo an amputation every year, resulting in 300 to 500 amputations per day; this amputation rate also will contribute to the market's growth.

Orthopedic prosthetics are artificial devices that replace missing body parts. These artificial limbs help patients/users with lost body parts (limbs) to function efficiently and resemble natural limbs. The lost parts could result from diseases, surgical removal, congenital conditions, trauma, or disabling illness.

The rising number of road accidents and increasing disability rates worldwide are also expected to drive the market's expansion but the high cost of these products could limit growth.

The orthopedic prosthetic devices sector is segmented into product, technique, and end user. The market is categorized into lower extremity prosthetics, upper extremity prosthetics, sockets, and other products. The lower extremity prosthetics segment is expected to maintain its dominance throughout 2022-2030. Also, the demand for upper extremist prosthetics is increasing owing to the rising number of spinal injuries.

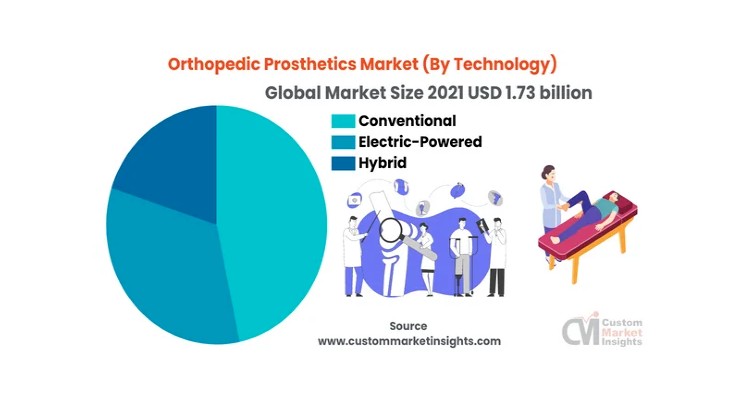

Rising diabetes and obesity rates globally will increase demand for lower extremity prosthetics. Based on technique, the electric-powered segment witnessed exponential growth from 2022 to 2030. By end users, the hospital's segment is expected to witness a high CAGR during the forecast period.

North America dominated the sector last year, accounting for more than 35% of the worldwide market share. The continent is expected to continue its dominance throughout the rest of this decade due to the presence of major players, significant investments in R&D, rising healthcare spending, and supportive reimbursement policies from the federal government.

The increasing number of sports injuries and rising occurrence of osteosarcoma are anticipated to drive demand for orthopedic prosthetic devices. The U.S. healthcare system also focuses on providing high-quality care and value-added services, expected to accelerate the demand shortly.

The Asia Pacific region is experiencing tremendous growth. Factors driving the market include rising diabetes cases, increasing road accidents, and favorable government initiatives in various economies. In 2018, an Asian Prosthetic and Orthotics meeting was held in Thailand to encourage cooperation among the area's economies and discuss relevant issues concerning prosthetics and orthotics.

Major market players are focused on introducing advanced medical devices that offer improved efficiency and patient compliance, expanding their portfolio and attaining a competitive edge. Additionally, increasing awareness about the advantages of advanced orthopedic prosthetic devices is boosting the market's growth.

Key market players include Ossur, B. Braun Melsungen AG, Smith+Nephew, Johnson & Johnson, Exatech Inc., Hanger Inc., Touch Bionics Inc., Howard Orthopaedics Inc., Medtronic Spinal, Globus Medical, Wishbone Medical, OrthoPediatrics, Arthrex, Pega Medical, Integra Lifesciences, Advanced Arm Dynamics, DJO Global, and others.

Custom Market Insights estimates the market value at approximately $1.96 billion this year and expects it to expand 9.5% annually to reach $3.97 billion by 2030, thanks to a projected increase in accidental injuries and trauma cases. Accidental injuries and trauma can result from sports injuries, medical complications, road accidents, and work-related injuries. Most of these accidents require prosthetics or amputations device to replace the lost body part. Around 2.1 million U.S. residents are living with limb loss, and that number is expected to double by 2050. Nearly 185,000 U.S. residents undergo an amputation every year, resulting in 300 to 500 amputations per day; this amputation rate also will contribute to the market's growth.

Orthopedic prosthetics are artificial devices that replace missing body parts. These artificial limbs help patients/users with lost body parts (limbs) to function efficiently and resemble natural limbs. The lost parts could result from diseases, surgical removal, congenital conditions, trauma, or disabling illness.

The rising number of road accidents and increasing disability rates worldwide are also expected to drive the market's expansion but the high cost of these products could limit growth.

The orthopedic prosthetic devices sector is segmented into product, technique, and end user. The market is categorized into lower extremity prosthetics, upper extremity prosthetics, sockets, and other products. The lower extremity prosthetics segment is expected to maintain its dominance throughout 2022-2030. Also, the demand for upper extremist prosthetics is increasing owing to the rising number of spinal injuries.

Rising diabetes and obesity rates globally will increase demand for lower extremity prosthetics. Based on technique, the electric-powered segment witnessed exponential growth from 2022 to 2030. By end users, the hospital's segment is expected to witness a high CAGR during the forecast period.

North America dominated the sector last year, accounting for more than 35% of the worldwide market share. The continent is expected to continue its dominance throughout the rest of this decade due to the presence of major players, significant investments in R&D, rising healthcare spending, and supportive reimbursement policies from the federal government.

The increasing number of sports injuries and rising occurrence of osteosarcoma are anticipated to drive demand for orthopedic prosthetic devices. The U.S. healthcare system also focuses on providing high-quality care and value-added services, expected to accelerate the demand shortly.

The Asia Pacific region is experiencing tremendous growth. Factors driving the market include rising diabetes cases, increasing road accidents, and favorable government initiatives in various economies. In 2018, an Asian Prosthetic and Orthotics meeting was held in Thailand to encourage cooperation among the area's economies and discuss relevant issues concerning prosthetics and orthotics.

Major market players are focused on introducing advanced medical devices that offer improved efficiency and patient compliance, expanding their portfolio and attaining a competitive edge. Additionally, increasing awareness about the advantages of advanced orthopedic prosthetic devices is boosting the market's growth.

Key market players include Ossur, B. Braun Melsungen AG, Smith+Nephew, Johnson & Johnson, Exatech Inc., Hanger Inc., Touch Bionics Inc., Howard Orthopaedics Inc., Medtronic Spinal, Globus Medical, Wishbone Medical, OrthoPediatrics, Arthrex, Pega Medical, Integra Lifesciences, Advanced Arm Dynamics, DJO Global, and others.