Ali Madani, Founder and Managing Partner, Avicenne Medical05.26.22

The future of orthopedic implants is inextricably linked to surgical robotics, which are set to improve clinical results. This is why implant manufacturers are looking to integrate robotic systems into their product offering. The following article provides a history of this trend and what is predicted for it.

In the late 1990s, major orthopedic implant manufacturers began offering navigation systems that allowed surgeons to know the position in space of a part of the patient’s body in relation to the instruments. The objective was to define the angles and locations of the cuts.

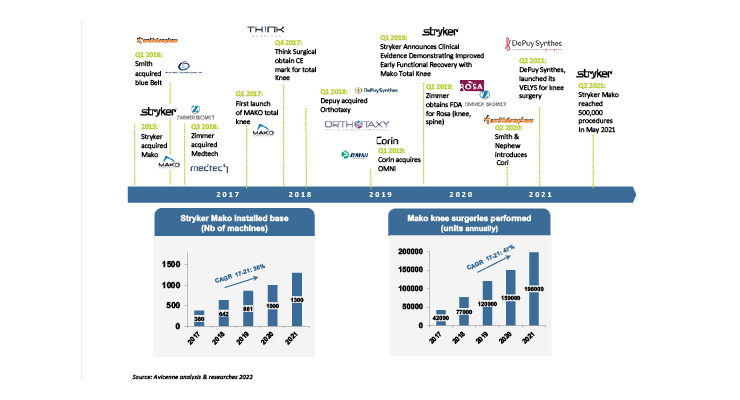

In 2006, U.S. company Mako Surgical distinguished itself by developing a 3D model based on CT scans of the patient to guide the arm of a robot during cutting and drilling operations on a skeleton. Then, in 2013, Stryker acquired Mako for $1.6 billion and, in 2017, launched the primary application for robotic orthopedics: total knee replacement.

Despite the high cost of acquiring the system (about $1 million) and the time required to learn and set up the robot, many Mako machines have been installed and their numbers are growing rapidly. Knee replacement surgeons are in the vanguard of the development of robotic operations.

With Stryker’s success and market share gains, the other orthopedic majors are seeking solutions to compete (Figure 1). They are all looking to launch, acquire, and/or develop robotic systems. Smith+Nephew, which bought Blue Belt Technology (announced in 2015), launched the Navio robot in 2016.

In the same year, Zimmer Biomet acquired the French-based company Medtech, originally developing a robotic system for spine surgery. From that point, Zimmer Biomet began transitioning the solution for the knee and obtained U.S. FDA approval in 2019.

For its part, DePuy Synthes acquired Orthotaxy, another company based in the Rhône-Alpes region of France, to eventually design the small Velys robot that it subsequently launched on the market in 2021.

A new turning point emerged with the company Think Surgical, which is developing an open platform that can be used by different companies, especially small ones that do not have the means to develop a proprietary system. Spine specialists such as Medtronic, NuVasive, and Globus are also developing robotic systems for spinal surgery.

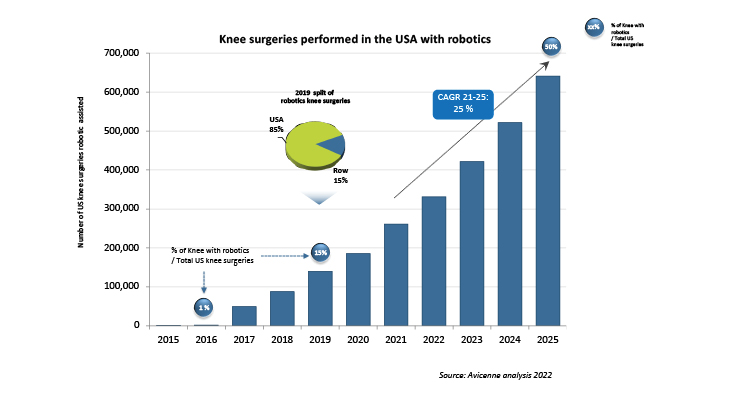

We can already speak of a mass market for orthopedic robotics in the United States, which accounts for 85 percent of robotic knee procedures worldwide. In Europe, the United Kingdom and Italy are the two countries where robots are used the most. Some hospitals there have made robotics their flagship. The Spire orthopedic center in Manchester alone announced it has performed more than 1,000 robotic knee surgeries.

Elsewhere, the Chinese company Tinavi is developing a robot for its local market and recently announced 20,000 robotic surgeries performed in the last few years.

Stryker had estimated the market for robotic systems—robots, maintenance, and consumables—for orthopedics would be $1 billion by 2021. Zimmer Biomet, meanwhile, announced that by the last quarter of 2021, knee procedures performed with the Rosa robot had reached 10 percent of all total knee replacements performed by the group. Avicenne Medical forecasts show in the United States—driven by Stryker, Zimmer Biomet, and the recent entrant, DePuy Synthes—nearly half of all knee implant surgeries in 2025 will be performed with the help of a robot.

While the industry has no doubt robotics will grow in the short and medium term in the United States, its evolution in other geographical regions, particularly in Europe, will depend on clinical studies demonstrating long-term benefits for patients, and on lower prices for acquisition and use.

Ali Madani is the founder and managing partner of Avicenne Medical, based in Paris, France. For more than 30 years, the firm has been advising medical device companies and their suppliers—especially in the orthopedic sector—on strategy, geographic expansion, innovation, and how to achieve profitable growth. Madani can be reached at a.madani@avicenne.com.

In the late 1990s, major orthopedic implant manufacturers began offering navigation systems that allowed surgeons to know the position in space of a part of the patient’s body in relation to the instruments. The objective was to define the angles and locations of the cuts.

In 2006, U.S. company Mako Surgical distinguished itself by developing a 3D model based on CT scans of the patient to guide the arm of a robot during cutting and drilling operations on a skeleton. Then, in 2013, Stryker acquired Mako for $1.6 billion and, in 2017, launched the primary application for robotic orthopedics: total knee replacement.

Stryker Leads the Way

In only a few years, use of the Mako system has become widespread, primarily in the United States. Surgeons now have at their disposal a device precise to 1.0 mm for positioning in space and to 1.0 degree for the cutting angles. This solution has become very popular with surgeons and clinics, who want to stand out from their competitors and modernize their image. In addition, by using robots, the practitioner feels better protected legally in the rare event of an incident.Despite the high cost of acquiring the system (about $1 million) and the time required to learn and set up the robot, many Mako machines have been installed and their numbers are growing rapidly. Knee replacement surgeons are in the vanguard of the development of robotic operations.

With Stryker’s success and market share gains, the other orthopedic majors are seeking solutions to compete (Figure 1). They are all looking to launch, acquire, and/or develop robotic systems. Smith+Nephew, which bought Blue Belt Technology (announced in 2015), launched the Navio robot in 2016.

In the same year, Zimmer Biomet acquired the French-based company Medtech, originally developing a robotic system for spine surgery. From that point, Zimmer Biomet began transitioning the solution for the knee and obtained U.S. FDA approval in 2019.

For its part, DePuy Synthes acquired Orthotaxy, another company based in the Rhône-Alpes region of France, to eventually design the small Velys robot that it subsequently launched on the market in 2021.

A new turning point emerged with the company Think Surgical, which is developing an open platform that can be used by different companies, especially small ones that do not have the means to develop a proprietary system. Spine specialists such as Medtronic, NuVasive, and Globus are also developing robotic systems for spinal surgery.

Already a Mass Market in the U.S.

Whereas in 2015, knee implant surgeries using a robot accounted for fewer than 1 percent of procedures in the United States, that ratio in 2019 was 15 percent (Figure 2). Approximately 85 percent of the robots used in these operations are from Stryker.We can already speak of a mass market for orthopedic robotics in the United States, which accounts for 85 percent of robotic knee procedures worldwide. In Europe, the United Kingdom and Italy are the two countries where robots are used the most. Some hospitals there have made robotics their flagship. The Spire orthopedic center in Manchester alone announced it has performed more than 1,000 robotic knee surgeries.

Elsewhere, the Chinese company Tinavi is developing a robot for its local market and recently announced 20,000 robotic surgeries performed in the last few years.

Stryker had estimated the market for robotic systems—robots, maintenance, and consumables—for orthopedics would be $1 billion by 2021. Zimmer Biomet, meanwhile, announced that by the last quarter of 2021, knee procedures performed with the Rosa robot had reached 10 percent of all total knee replacements performed by the group. Avicenne Medical forecasts show in the United States—driven by Stryker, Zimmer Biomet, and the recent entrant, DePuy Synthes—nearly half of all knee implant surgeries in 2025 will be performed with the help of a robot.

While the industry has no doubt robotics will grow in the short and medium term in the United States, its evolution in other geographical regions, particularly in Europe, will depend on clinical studies demonstrating long-term benefits for patients, and on lower prices for acquisition and use.

Ali Madani is the founder and managing partner of Avicenne Medical, based in Paris, France. For more than 30 years, the firm has been advising medical device companies and their suppliers—especially in the orthopedic sector—on strategy, geographic expansion, innovation, and how to achieve profitable growth. Madani can be reached at a.madani@avicenne.com.