08.15.17

$2.9 Billion

KEY EXECUTIVES:

Omar Ishrak, Chairman and CEO

Karen L. Parkhill, Exec. VP and Chief Financial Officer

Gary L. Ellis, Exec. VP of Global Operations and Information Technology

Bradley E. Lerman, Sr. VP, General Counsel and Corporate Secretary

Geoffrey S. Martha, Exec. VP and President, Restorative Therapies Group

Robert ten Hoedt, Exec. VP and President, EMEA

NO. OF EMPLOYEES: 5,600

GLOBAL HEADQUARTERS: Memphis, Tenn.

One of the most beloved movie endings ever filmed almost never made it onscreen.

The script for the 1971 musical fantasy “Willy Wonka and the Chocolate Factory” originally ended with Grandpa Joe shouting, “Yippie!” and then fading to black. But Emmy award-winning director Mel Stuart wanted a better closing line, and reportedly phoned writer David Seltzer from the set to request a more memorable finale.

Seltzer could only come up with one idea, though it was a bit cliché. In the film’s final scene—cherished by millions of fans worldwide—the eccentric title character announces he is giving his entire factory to Charlie Bucket, a kind-hearted, honest, but poor boy who lives with his widowed mother and four bedridden grandparents in the slums of an unnamed European city. As Charlie’s disbelief turns to gratitude, Wonka hugs the boy, then tells him, “But Charlie, don’t forget what happened to the man who suddenly got everything he always wanted.”

“What happened?” Charlie asks, amazed.

“He lived happily ever after,” Wonka replies, smiling.

Of course he did. It is a movie, after all.

Hollywood is notorious for its happy endings, but such closure is not as readily found off-screen. Fairy tales and their all-is-well finales are pure fiction; the real world doesn’t work that way—it’s cold, inconsistent, and oftentimes unfair. It offers no guarantees on contentment.

Joy can be particularly elusive in business, even for companies that follow Wonka’s guide to eternal euphoria. Apple Inc.’s Cinderella-like evolution, for example, should theoretically ensure the multinational technology firm lives happily ever after. But since ascending to the Most Valuable Company throne six years ago, Apple has grappled with a litany of serious issues—among them the death of co-founder Steve Jobs, concerns about its innovative prowess, declining iPhone sales, underwhelming products (think Apple TV and the Apple watch), and stagnating stock value.

Certainly not the enchanted future Tinseltown would have dreamed up.

Medtronic plc is experiencing similar dream disillusionment as it settles into its new role as the planet’s top medtech firm. Bolstered by the integration of a historic $50 billion acquisition, Medtronic garnered $28.8 billion in fiscal 2016 sales to surpass rival Johnson & Johnson for top industry billing and bragging rights. It was a crowning achievement, as transformative for the company as it was impressive in both size and scope.

Perhaps more important than the prestige of Medtronic’s achievement, however, is the opportunity it provides the 68-year-old multinational firm to improve healthcare worldwide.“...the full integration of Covidien—acquired in late FY2015—has greatly expanded our global reach and impact,” Chairman and CEO Omar Ishrak wrote in his introduction to the 2016 Integrated Performance Report. “More than 65 million people benefited from Medtronic technologies—two every second—as we helped our customers deliver more seamless, integrated care for patients across the healthcare continuum.”

Two people every second.

Not too shabby for an enterprise that began in a 600-square-foot-garage and grossed a mere $8 in its first month of operation.

Indeed, Medtronic’s journey from humble beginnings to world domination is a remarkable feat that deserves recognition. On the Silver Screen, it would represent the perfect ending to the perfect rags-to-riches story, save for the post-credit affirmation of the company’s everlasting joy.

But perfection is an anomaly in the real world, muddling efforts by true larger-than-life entities like Apple and Medtronic to secure a happy ending. Certainly, Medtronic’s prospects for eternal bliss dimmed moderately in FY16 due to product recalls, a consent decree, slumping spinal and neuromodulation sales, and lingering discord over its controversial bone fusion technology.

The spine division extended its multi-year sales slide in FY16 (period ended April 29, 2016), losing 2 percent in revenue from the previous fiscal term to drop to $2.92 billion. Medtronic attributed the declivity to dwindling core spine and interventional revenue, both of which succumbed to global pricing pressures—a culprit that also undermined much of the single-digit growth that occurred in the U.S. core spine market. Even with the handicap, however, core spine still experienced “sequential improvement” in its overall growth rate, due largely to incremental revenue from differentiated oblique lateral interbody fusion procedures, new products, and the company’s Speed to Scale initiative, a program designed to accelerate innovation and deployment of new products and procedures.

ANALYST INSIGHTS: Medtronic continues to deliver on the promises made at the time of the Covidien acquisition. The $800 million annual savings has largely come to pass. The company has market share leadership in a majority of categories of high-value devices. While the transition was bumpy for some divisions and unclear for their supply chain partners, Medtronic has made it through the acquisition to the other side. Watch for additional moves to ensure dominance in their selected markets, along with a willingness to shed the remainder of their non-strategic assets.

Among the growth engendering products were the CD Horizon Solera Voyager Spinal System and Medtronic’s platform of PTC Interbody fusion devices. The latter product line—comprised of titanium and the ever-popular material polyetheretherketone (PEEK)—is designed to treat back pain caused by spinal cord or nerve root compression, while the CD Horizon Solera system (launched in July 2015) is designed specifically for minimally invasive spinal surgery.

Available worldwide, the CD Horizon Solera Voyager System expands upon the transforaminal lumbar interbody fusion procedure by offering multiple, minimally invasive rod insertion options and enabling a seamless 3D-navigated surgical experience. The product gives surgeons the flexibility to use either a percutaneous or Wiltse minimally invasive approach for rod insertion, depending upon their preference. The system also features a low-profile, extended-tab screw with inner threading, which eases rod insertion and facilitates rod reduction.

“This system represents our commitment to take minimally invasive techniques and 3D-navigated surgery even further and develop solutions with clinical and economic value,” Doug King, president of Medtronic’s spinal business and senior vice president, said when the Solera system debuted.

Solid bone morphogenetic protein (BMP) growth in the United States partly neutralized the core spine and interventional sales shortfall, but that gain was itself negated by falling BMP revenue overseas due to an InductOs shipping hold in Europe. BMP’s strong American showing likely benefitted by U.S. regulators’ December 2015 approval of Infuse Bone Graft for three new spinal surgery indications: single-level fusion OLIF51 procedures from the L5 vertebra to S1 with Medtronic’s PEEK Perimeter implant; OLIF25 fusions from L2 to L5 using the PEEK Clydesdale implant; and ALIF procedures from L2 to S1 using the Perimeter device. The expanded indications represent the first U.S. Food and Drug Administration (FDA)-sanctioned use of Infuse for lower back surgery using plastic rather than titanium components.

The FDA’s blessing of Infuse, however, failed to quell the controversy that continued to plague the bone-growth protein product in FY16. A front-page story in the Minneapolis Star Tribune last April detailed the circumstances surrounding Medtronic’s “misfiled” report on treatment complications with its bone fusion product, Infuse. The newspaper claimed the company informed the FDA of over 1,000 Infuse-related “adverse events” more than five years after they occurred.

ANALYST INSIGHTS: Omar Ishrak has made a positive impact on revenue and EBITDA thru “pulling the right levers” since taking over Medtronic. Acquisitions, Cash-Flow and Portfolio Management will continue to be a key emphasis in the months to come. Watch for Medtronic to continue to defend its market position by furthering its leadership in “risk-sharing” agreements with its customers.

Medtronic, naturally, criticized the article, claiming it made “false insinuations” and failed to include important information about a retrospective chart review (RCR) of Infuse data and the company’s remedial actions. “...the article suggests Medtronic attempted to conceal information about the RCR, including information about adverse events reported in the data. This suggestion is false...” the company contended in direct response to the Star Tribune story. “Medtronic has acknowledged that at the time the RCR was discontinued back in 2008, it was not properly archived and the information collected was not fully assessed for reportability to the FDA. We have taken a number of steps to update our clinical policies and our training to enhance our reporting practices.”

While hardly overblown, the company’s Star Tribune spat nevertheless attracted the attention of U.S. Sen. Al Franken (D-Minn.), a member of the Senate Health, Education, Labor and Pensions Committee, and ardent medtech industry advocate. In a surprising departure from past viewpoints, Franken asked both Medtronic and the FDA for detailed information about patient injuries, including the severity of the trauma and their relationship to Infuse. He also requested an accounting of approved and off-label treatment uses.

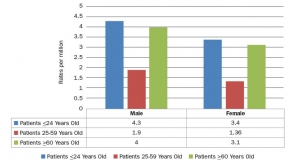

In late December 2015, the U.S. Food and Drug Administration cleared Medtronic’s controversial Infuse Bone Graft biologic product for lower back surgery for use with plastic rather than titanium spinal components. The agency’s decision gave surgeons three additional FDA-approved procedures, according to the company. Image courtesy of Medtronic plc.

“The information portrayed in the [Star Tribune] article suggests that Medtronic conducted a study of its Infuse device, and for five years, failed to report thousands of complications related to the device to the FDA,” Franken wrote in an April 12, 2016, letter to the FDA outlining his requests. “This lack of information potentially skewed the risk profile of the device, which may have affected the treatment of thousands of additional patients.”

Franken’s assertion is at the crux of a new class-action lawsuit filed against Medtronic by thousands of patients treated with Infuse. The suit alleges product liability and fraud over the company’s Infuse Bone Graft LT-Cage Lumbar Tapered Fusion Device System, a thimble-like titanium product that keeps bone graft at the fusion site, maintains proper height between vertebrae, and stabilizes the spine during fusion. Court documents accuse Medtronic of employing an illegal, false, and deceptive marketing scheme to promote the sale of Infuse for off-label uses.

With a happy ending in Spine marred by declining revenue and recurrent Infuse controversy, Medtronic was forced to look elsewhere for a fairy tale-like finale to its fiscal 2016 finances. And it found such closure in all other product franchises.

In fact, the gains realized in Medtronic’s seven other reporting divisions more than compensated for losses in Spine and Neuromodulation, thanks to the full integration of Covidien. In the Restorative Therapies Group alone, the more than four-fold increase in Neurovascular net sales (345 percent to $587 million) single-handedly annihilated any negative impact the two backsliding sectors may have had on overall company revenue, which mushroomed 42.3 percent. Likewise, the losses had no effect on Medtronic’s FY16 net income or operating profit, which surged 32.2 percent and 40.5 percent respectively.

ANALYST INSIGHTS: What’s next? With the Covidien acquisition now three years away, and after shedding the Covidien legacy medical supplies business, what is the device behemoth’s next move? Most likely more acquisitions, maybe even another blockbuster. Stay tuned.

One of four product franchises formed from the Covidien acquisition, the Neurovascular division outshined its Group brethren through strong sales of the Solitaire FR mechanical thrombectomy device, Pipeline Flex (United States and Japan), and Pipeline Flex with Shield technology (Europe). The Pipeline Flex is a flow diversion device used to treat large and giant wide-necked brain aneurysms that are attached to parent vessels measuring between 2.5 and 5 mm in diameter; the version with Shield technology includes a surface synthetic biocompatible polymer.

KEY EXECUTIVES:

Omar Ishrak, Chairman and CEO

Karen L. Parkhill, Exec. VP and Chief Financial Officer

Gary L. Ellis, Exec. VP of Global Operations and Information Technology

Bradley E. Lerman, Sr. VP, General Counsel and Corporate Secretary

Geoffrey S. Martha, Exec. VP and President, Restorative Therapies Group

Robert ten Hoedt, Exec. VP and President, EMEA

NO. OF EMPLOYEES: 5,600

GLOBAL HEADQUARTERS: Memphis, Tenn.

One of the most beloved movie endings ever filmed almost never made it onscreen.

The script for the 1971 musical fantasy “Willy Wonka and the Chocolate Factory” originally ended with Grandpa Joe shouting, “Yippie!” and then fading to black. But Emmy award-winning director Mel Stuart wanted a better closing line, and reportedly phoned writer David Seltzer from the set to request a more memorable finale.

Seltzer could only come up with one idea, though it was a bit cliché. In the film’s final scene—cherished by millions of fans worldwide—the eccentric title character announces he is giving his entire factory to Charlie Bucket, a kind-hearted, honest, but poor boy who lives with his widowed mother and four bedridden grandparents in the slums of an unnamed European city. As Charlie’s disbelief turns to gratitude, Wonka hugs the boy, then tells him, “But Charlie, don’t forget what happened to the man who suddenly got everything he always wanted.”

“What happened?” Charlie asks, amazed.

“He lived happily ever after,” Wonka replies, smiling.

Of course he did. It is a movie, after all.

Hollywood is notorious for its happy endings, but such closure is not as readily found off-screen. Fairy tales and their all-is-well finales are pure fiction; the real world doesn’t work that way—it’s cold, inconsistent, and oftentimes unfair. It offers no guarantees on contentment.

Joy can be particularly elusive in business, even for companies that follow Wonka’s guide to eternal euphoria. Apple Inc.’s Cinderella-like evolution, for example, should theoretically ensure the multinational technology firm lives happily ever after. But since ascending to the Most Valuable Company throne six years ago, Apple has grappled with a litany of serious issues—among them the death of co-founder Steve Jobs, concerns about its innovative prowess, declining iPhone sales, underwhelming products (think Apple TV and the Apple watch), and stagnating stock value.

Certainly not the enchanted future Tinseltown would have dreamed up.

Medtronic plc is experiencing similar dream disillusionment as it settles into its new role as the planet’s top medtech firm. Bolstered by the integration of a historic $50 billion acquisition, Medtronic garnered $28.8 billion in fiscal 2016 sales to surpass rival Johnson & Johnson for top industry billing and bragging rights. It was a crowning achievement, as transformative for the company as it was impressive in both size and scope.

Perhaps more important than the prestige of Medtronic’s achievement, however, is the opportunity it provides the 68-year-old multinational firm to improve healthcare worldwide.“...the full integration of Covidien—acquired in late FY2015—has greatly expanded our global reach and impact,” Chairman and CEO Omar Ishrak wrote in his introduction to the 2016 Integrated Performance Report. “More than 65 million people benefited from Medtronic technologies—two every second—as we helped our customers deliver more seamless, integrated care for patients across the healthcare continuum.”

Two people every second.

Not too shabby for an enterprise that began in a 600-square-foot-garage and grossed a mere $8 in its first month of operation.

Indeed, Medtronic’s journey from humble beginnings to world domination is a remarkable feat that deserves recognition. On the Silver Screen, it would represent the perfect ending to the perfect rags-to-riches story, save for the post-credit affirmation of the company’s everlasting joy.

But perfection is an anomaly in the real world, muddling efforts by true larger-than-life entities like Apple and Medtronic to secure a happy ending. Certainly, Medtronic’s prospects for eternal bliss dimmed moderately in FY16 due to product recalls, a consent decree, slumping spinal and neuromodulation sales, and lingering discord over its controversial bone fusion technology.

The spine division extended its multi-year sales slide in FY16 (period ended April 29, 2016), losing 2 percent in revenue from the previous fiscal term to drop to $2.92 billion. Medtronic attributed the declivity to dwindling core spine and interventional revenue, both of which succumbed to global pricing pressures—a culprit that also undermined much of the single-digit growth that occurred in the U.S. core spine market. Even with the handicap, however, core spine still experienced “sequential improvement” in its overall growth rate, due largely to incremental revenue from differentiated oblique lateral interbody fusion procedures, new products, and the company’s Speed to Scale initiative, a program designed to accelerate innovation and deployment of new products and procedures.

ANALYST INSIGHTS: Medtronic continues to deliver on the promises made at the time of the Covidien acquisition. The $800 million annual savings has largely come to pass. The company has market share leadership in a majority of categories of high-value devices. While the transition was bumpy for some divisions and unclear for their supply chain partners, Medtronic has made it through the acquisition to the other side. Watch for additional moves to ensure dominance in their selected markets, along with a willingness to shed the remainder of their non-strategic assets.

—Tony Freeman, President, AS Freeman Advisors LLC

Among the growth engendering products were the CD Horizon Solera Voyager Spinal System and Medtronic’s platform of PTC Interbody fusion devices. The latter product line—comprised of titanium and the ever-popular material polyetheretherketone (PEEK)—is designed to treat back pain caused by spinal cord or nerve root compression, while the CD Horizon Solera system (launched in July 2015) is designed specifically for minimally invasive spinal surgery.

Available worldwide, the CD Horizon Solera Voyager System expands upon the transforaminal lumbar interbody fusion procedure by offering multiple, minimally invasive rod insertion options and enabling a seamless 3D-navigated surgical experience. The product gives surgeons the flexibility to use either a percutaneous or Wiltse minimally invasive approach for rod insertion, depending upon their preference. The system also features a low-profile, extended-tab screw with inner threading, which eases rod insertion and facilitates rod reduction.

“This system represents our commitment to take minimally invasive techniques and 3D-navigated surgery even further and develop solutions with clinical and economic value,” Doug King, president of Medtronic’s spinal business and senior vice president, said when the Solera system debuted.

Solid bone morphogenetic protein (BMP) growth in the United States partly neutralized the core spine and interventional sales shortfall, but that gain was itself negated by falling BMP revenue overseas due to an InductOs shipping hold in Europe. BMP’s strong American showing likely benefitted by U.S. regulators’ December 2015 approval of Infuse Bone Graft for three new spinal surgery indications: single-level fusion OLIF51 procedures from the L5 vertebra to S1 with Medtronic’s PEEK Perimeter implant; OLIF25 fusions from L2 to L5 using the PEEK Clydesdale implant; and ALIF procedures from L2 to S1 using the Perimeter device. The expanded indications represent the first U.S. Food and Drug Administration (FDA)-sanctioned use of Infuse for lower back surgery using plastic rather than titanium components.

The FDA’s blessing of Infuse, however, failed to quell the controversy that continued to plague the bone-growth protein product in FY16. A front-page story in the Minneapolis Star Tribune last April detailed the circumstances surrounding Medtronic’s “misfiled” report on treatment complications with its bone fusion product, Infuse. The newspaper claimed the company informed the FDA of over 1,000 Infuse-related “adverse events” more than five years after they occurred.

ANALYST INSIGHTS: Omar Ishrak has made a positive impact on revenue and EBITDA thru “pulling the right levers” since taking over Medtronic. Acquisitions, Cash-Flow and Portfolio Management will continue to be a key emphasis in the months to come. Watch for Medtronic to continue to defend its market position by furthering its leadership in “risk-sharing” agreements with its customers.

—Dave Sheppard, Co-Founder and Principal, MedWorld Advisors

Medtronic, naturally, criticized the article, claiming it made “false insinuations” and failed to include important information about a retrospective chart review (RCR) of Infuse data and the company’s remedial actions. “...the article suggests Medtronic attempted to conceal information about the RCR, including information about adverse events reported in the data. This suggestion is false...” the company contended in direct response to the Star Tribune story. “Medtronic has acknowledged that at the time the RCR was discontinued back in 2008, it was not properly archived and the information collected was not fully assessed for reportability to the FDA. We have taken a number of steps to update our clinical policies and our training to enhance our reporting practices.”

While hardly overblown, the company’s Star Tribune spat nevertheless attracted the attention of U.S. Sen. Al Franken (D-Minn.), a member of the Senate Health, Education, Labor and Pensions Committee, and ardent medtech industry advocate. In a surprising departure from past viewpoints, Franken asked both Medtronic and the FDA for detailed information about patient injuries, including the severity of the trauma and their relationship to Infuse. He also requested an accounting of approved and off-label treatment uses.

In late December 2015, the U.S. Food and Drug Administration cleared Medtronic’s controversial Infuse Bone Graft biologic product for lower back surgery for use with plastic rather than titanium spinal components. The agency’s decision gave surgeons three additional FDA-approved procedures, according to the company. Image courtesy of Medtronic plc.

Franken’s assertion is at the crux of a new class-action lawsuit filed against Medtronic by thousands of patients treated with Infuse. The suit alleges product liability and fraud over the company’s Infuse Bone Graft LT-Cage Lumbar Tapered Fusion Device System, a thimble-like titanium product that keeps bone graft at the fusion site, maintains proper height between vertebrae, and stabilizes the spine during fusion. Court documents accuse Medtronic of employing an illegal, false, and deceptive marketing scheme to promote the sale of Infuse for off-label uses.

With a happy ending in Spine marred by declining revenue and recurrent Infuse controversy, Medtronic was forced to look elsewhere for a fairy tale-like finale to its fiscal 2016 finances. And it found such closure in all other product franchises.

In fact, the gains realized in Medtronic’s seven other reporting divisions more than compensated for losses in Spine and Neuromodulation, thanks to the full integration of Covidien. In the Restorative Therapies Group alone, the more than four-fold increase in Neurovascular net sales (345 percent to $587 million) single-handedly annihilated any negative impact the two backsliding sectors may have had on overall company revenue, which mushroomed 42.3 percent. Likewise, the losses had no effect on Medtronic’s FY16 net income or operating profit, which surged 32.2 percent and 40.5 percent respectively.

ANALYST INSIGHTS: What’s next? With the Covidien acquisition now three years away, and after shedding the Covidien legacy medical supplies business, what is the device behemoth’s next move? Most likely more acquisitions, maybe even another blockbuster. Stay tuned.

—Mark Bonifacio, Founder & President, Bonifacio Consulting Services

One of four product franchises formed from the Covidien acquisition, the Neurovascular division outshined its Group brethren through strong sales of the Solitaire FR mechanical thrombectomy device, Pipeline Flex (United States and Japan), and Pipeline Flex with Shield technology (Europe). The Pipeline Flex is a flow diversion device used to treat large and giant wide-necked brain aneurysms that are attached to parent vessels measuring between 2.5 and 5 mm in diameter; the version with Shield technology includes a surface synthetic biocompatible polymer.