Maria Shepherd, President and Founder, Medi-Vantage11.13.23

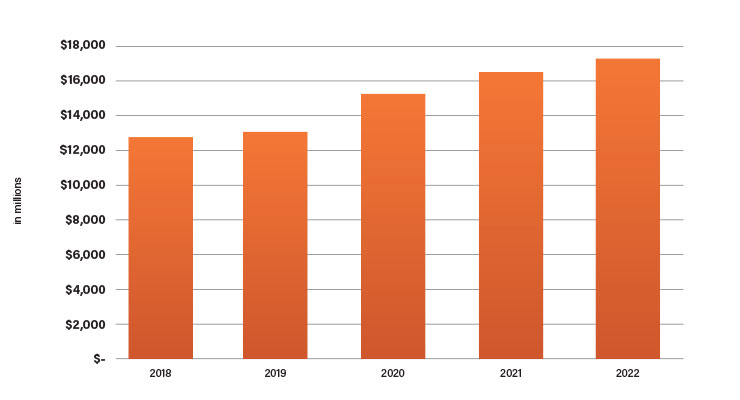

In 2021, U.S. healthcare costs rose to $4.3 trillion, or 18.3% of the U.S. Gross Domestic Product.1 A stealthy disruptor within medtech is the consumer medical device retail segment, which grew from almost $13 billion in 2018 to $17.1 billion in 2022 (Table 1).2 These revenues include the traditional categories of oral care devices, contact lens care, feminine care, first aid devices, medical accessories, adult incontinence, pain relieving devices, and sexual health.2

Consumer healthcare spending is increasing, and healthcare buyers are requiring more convenience and high- quality care in their communities. The pressure of healthcare consumerism is good for business. Involved consumers have the power to drive improved quality and reduced costs, and medtech companies and retail healthcare can address this in their business models.

These trends have stimulated growth in retail healthcare. Disruptors are penetrating the retail space with large investments and partnerships that are new and transforming the ecosystem of care. Clinics are located in stand-alone facilities, big-box retailers, pharmacies, and supermarkets. Growth over the last five years is reported to have been as high as 200%, in large part due to the pandemic (Table 2).3

DME is often needed by the same patients who need medication. Pharmacies have been adopting the strategy of providing medication dispensers using a more holistic strategy for patient care and recognize these adjacent spaces are good for their businesses, patients, and communities. For example, if the patient gets a script filled for albuterol, why not also sell them the nebulizer needed to administer this medication?

In the pain management space, orthopedic braces are another traditional DME category. These devices provide the support many injured patients need to help ensure a full recovery. In addition, orthopedic brace support helps reduce pain through stabilizing the injured anatomy and limiting motion.

TENS (transcutaneous electrical nerve stimulation) units are another pain management device. Their electrodes transmit electrical signals to the user’s nerves to impede the transmission of pain signals. TENS units are small, discreet, and can be worn by patients throughout the day. These devices have switches that allow the user to change the stimulation intensity, frequency, and duration.

Orthotics and orthopedic devices are a large category that includes posture support, footwear, splints, and braces. Some are reimbursable through Medicare or private pay insurance; however, patients may not always be able to get the specific devices they want. Also, it’s not just the elderly that buy DME products. Athletes are a large user of orthotic products, such as wrist splints and ankle braces.

The seismic growth of retail clinics is a double-edged sword of opportunity and challenge. For patients, retail clinics are a cost-effective, fast, and convenient alternative to traditional healthcare settings like the physician’s office. Retail clinics may also be a solution for lower-income or rural areas that have poor access to medical resources. However, there are also concerns about quality of care and the interruption of patient-physician relationships.

In a recent survey, a positive effect of retail healthcare on patients and conventional healthcare providers are less expensive healthcare at reduced costs, fewer barriers to healthcare access, fewer trips to the emergency room, and higher quality but more fragmented care.3

References

Maria Shepherd has more than 20 years of experience in marketing in small startups and top-tier companies. She founded Medi-Vantage, which provides marketing and business strategy for the medtech industry. She can be reached at mshepherd@medi-vantage.com. Visit her website at www.medi-vantage.com.

Consumer healthcare spending is increasing, and healthcare buyers are requiring more convenience and high- quality care in their communities. The pressure of healthcare consumerism is good for business. Involved consumers have the power to drive improved quality and reduced costs, and medtech companies and retail healthcare can address this in their business models.

These trends have stimulated growth in retail healthcare. Disruptors are penetrating the retail space with large investments and partnerships that are new and transforming the ecosystem of care. Clinics are located in stand-alone facilities, big-box retailers, pharmacies, and supermarkets. Growth over the last five years is reported to have been as high as 200%, in large part due to the pandemic (Table 2).3

New Categories of Retail Medical Devices

The durable medical equipment (DME) market may be in for a surprise when the local pharmacy starts penetrating their market share. The U.S. DME market size was valued at $59.7 billion in 2022 and is expected to grow at a CAGR of 5.7% from 2023 to 2030.4 This market is driven by the aging population and to thrive in a rapidly changing landscape, several retail pharmacies are adapting by adding DME to their shelves. This strategy is a good one for retail healthcare clinics that seek to build service and trust with their patients.DME is often needed by the same patients who need medication. Pharmacies have been adopting the strategy of providing medication dispensers using a more holistic strategy for patient care and recognize these adjacent spaces are good for their businesses, patients, and communities. For example, if the patient gets a script filled for albuterol, why not also sell them the nebulizer needed to administer this medication?

In the pain management space, orthopedic braces are another traditional DME category. These devices provide the support many injured patients need to help ensure a full recovery. In addition, orthopedic brace support helps reduce pain through stabilizing the injured anatomy and limiting motion.

TENS (transcutaneous electrical nerve stimulation) units are another pain management device. Their electrodes transmit electrical signals to the user’s nerves to impede the transmission of pain signals. TENS units are small, discreet, and can be worn by patients throughout the day. These devices have switches that allow the user to change the stimulation intensity, frequency, and duration.

Orthotics and orthopedic devices are a large category that includes posture support, footwear, splints, and braces. Some are reimbursable through Medicare or private pay insurance; however, patients may not always be able to get the specific devices they want. Also, it’s not just the elderly that buy DME products. Athletes are a large user of orthotic products, such as wrist splints and ankle braces.

The seismic growth of retail clinics is a double-edged sword of opportunity and challenge. For patients, retail clinics are a cost-effective, fast, and convenient alternative to traditional healthcare settings like the physician’s office. Retail clinics may also be a solution for lower-income or rural areas that have poor access to medical resources. However, there are also concerns about quality of care and the interruption of patient-physician relationships.

In a recent survey, a positive effect of retail healthcare on patients and conventional healthcare providers are less expensive healthcare at reduced costs, fewer barriers to healthcare access, fewer trips to the emergency room, and higher quality but more fragmented care.3

Where Are Retail Healthcare Clinics?

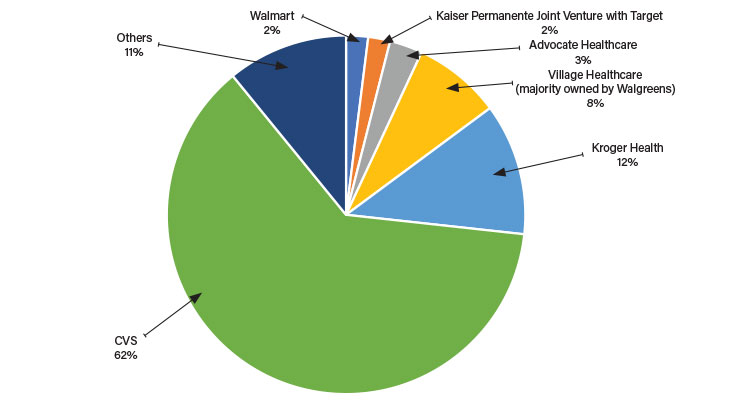

Until now, most retail healthcare clinics have been dominated by large retailers like Walgreens, CVS, and Walmart. The new trend in the past five years is for hospitals and health systems to try to regain market share by partnering with retail healthcare clinic chains or establishing their own to respond to the rising demand for patient-centric healthcare.3 According to the Definitive Healthcare report, in 2023, there were greater than 1,800 retail healthcare clinics in 44 U.S. states, most stationed in major metropolitan areas. Retail healthcare clinic claims volumes have grown substantially, estimated at greater than 200% since 2017 (Table 3).3Who Wins, Who Loses?

One negative impact to medtech may be in the reduction of trips to the emergency room. While this is good for the U.S. healthcare system based on reduced cost and clinician shortages, it is estimated that ED visits could be reduced by 3% to 13% for avoidable disorders and 6% to 12% for minor acute conditions from local communities. The ED is a significant customer for the medtech industry and a greater than 10% drop in revenues will affect us industry-wide. It is unclear if retail healthcare clinics will make up the difference; the scale of patient treatment is very different.The Medi-Vantage Perspective

Let’s face it, retail healthcare clinics are here to stay because they meet our basic unmet needs. Patients receive fast, accessible, low-cost, essential primary care, screening, and diagnostic services. Retail healthcare clinics are filling a gap in the U.S. healthcare system as we lurch toward the quadruple aim goals of improved patient care, population health, work-life balance of healthcare providers, and reduced costs. Many retail healthcare clinics are growing their services to include fundamental chronic care management services, pharmacies, and healthy foods. Do not ignore this channel; the role of retail healthcare clinics will continue to evolve in the face of challenges and opportunities to claim their space in the U.S. healthcare system, evolving to meet their goals and contribute to improved outcomes.References

Maria Shepherd has more than 20 years of experience in marketing in small startups and top-tier companies. She founded Medi-Vantage, which provides marketing and business strategy for the medtech industry. She can be reached at mshepherd@medi-vantage.com. Visit her website at www.medi-vantage.com.